GIFI

Gulf Island Fabrication, Inc. (GIFI)

Enterprise Value: (8.84)mm

Share Price: $4.04

—----------------

Strategy: Negative Enterprise Value

Strategy Description: This is a quantitative deep value strategy whereby investors purchase a basket of stocks that trade for an enterprise value under zero. For a brief primer, I recommend this article. In summary, the author’s backtest of an NEV strategy had an average return rate of 50.4%. While that number does not account for taxes and trading costs, and while average return is not the same as CAGR, 50.4% is compelling.

NEV stocks are the most steeply-discounted stocks available for purchase on a purely quantitative, balance sheet basis. With this strategy, an investor purchases a sufficiently diversified basket of these stocks with the expectation that the basket as a whole will perform well, disregarding the occasional poor performance of a single stock in the portfolio. The investor, in addition, is relatively unconcerned with the qualitative factors of any single stock. He may make predictions about the future performance of a company or industry, but he does not rely on these predictions.

—----------------

Basic Screening Criteria

Country: United States

I prefer to use deep value strategies with stocks in the developed world. In particular, I steer clear of Chinese equities. Corporate fraud is too common there, and I lack the sophistication to distinguish between real opportunities and fraudulent ones. If I were to develop a portfolio of developing-world stocks, I would probably take a broad-based approach, ensuring diversification across dozens of countries and hundreds of stocks. In the developed world, I feel comfortable sticking with a concentrated portfolio.

Market Cap and Exchange: 64.54mm, Nasdaq

Multiple studies (see “Stocks with Smaller Market Capitalizations”) have shown that value stocks with small market caps outperform their larger peers. I have also noticed anecdotally that the market gets more inefficient the smaller you get. In the competitive enterprise of capital allocation, it seems like any small-time individual investor who ignores the microcap space is giving up his single most powerful competitive advantage–his small size. You can find value in any corner of the market of course, but I have limited time, and I prefer to “fish where the fish are.” As a result, I limit my investable universe to stocks with a market cap of under $200mm. Within that microcap universe, I prefer stocks on the smaller end of the scale: sub-$50mm or even sub-$25mm. I also like OTC listings over exchange listings. Plenty of institutional and individual investors exclude OTC stocks as a class, and OTC listings are often excluded from screeners–both very good things for value-oriented contrarians.

Firm Type: Industrial

I exclude several types of firm from this strategy. I typically exclude financial firms from consideration, since they report financials differently from other firms. I may add financial firms to my portfolio on a case-by-case basis using other deep value strategies. For example, I may invest in a financial firm as part of a special situations strategy or a thrift conversion strategy. With the negative EV strategy, though, no financials. I also avoid firms that are known for a high burn rate, so I will eliminate firms in the oil/gas exploration and biotech spaces. These melting glaciers often trade at a discount to net cash for a good reason. Shell companies tend to have no revenue but do tend to have plenty of overhead that kills the value thesis, so I take these out of consideration. On an ad hoc basis, though, I will consider adding a shell company to the portfolio as a special situation play.

An old economy industrial firm like GIFI is a classic deep value stock, so I am in the right ballpark here.

—----------------

Business Summary

Gulf Island primarily serves the oil and natural gas industry. The company owns two properties southwest of New Orleans from which it operates in two segments–fabrication and shipbuilding.

The fabrication segment serves the energy sector (both onshore and offshore, both the oil and alternatives industries), other industrial companies, and the government (flood control projects).

The shipyard segment builds and services support vessels and drydocks, mostly for the oil and gas industry. This seems to be an undifferentiated, commodity-type industry. These are ships like tugboats and barges, a.k.a. uncomplex capital equipment.

As would be expected with a microcap heavy industry stock, customer concentration is high, with two customers accounting for 46% of FY’20 revenue. This is an unsexy business with unimpressive barriers to entry. The last few years have, of course, been unkind to the oil and gas industry.

GIFI has no recent coverage on VIC, and two SA articles from the last two years.

—----------------

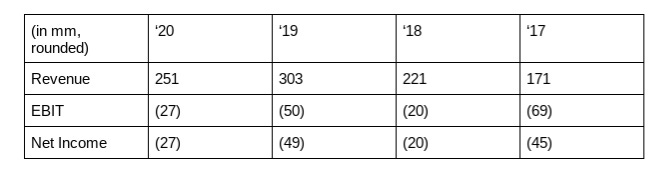

Income Snapshot

—----------------

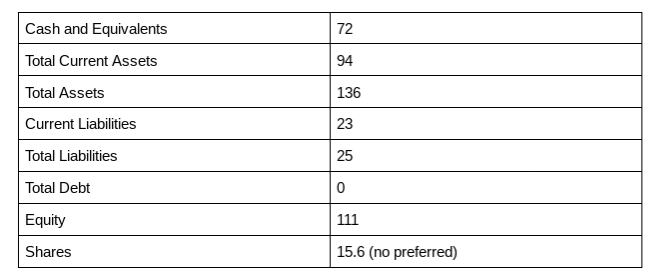

Balance Sheet Snapshot

Quarter Ending 9/30/21 (in mm, rounded)

—----------------

Criteria to Avoid a Value Trap

Stock Recently Traded at a Positive Enterprise Value

A stock which has traded at a negative enterprise value for an extended period of time would suggest that there may be a good reason for the negative EV valuation (e.g. suspected fraud, high cash burn, etc.). GIFI traded at a positive EV as recently as August.

Company Has a History of Profitability

I look for a positive GAAP net income sometime in recent history to offer me some reassurance that the company can remain solvent and that it won’t burn through its balance sheet. Obviously, GIFI has sustained massive losses, but with positive net income in 2016, it squeaks by.

Company Has not Diluted Shareholders to an Excessive Degree

Many apparent value stocks become much less appealing when you take a look at share count growth over the last few years. Of course, I would prefer to see a Graham-style value stock cannibalizing itself with buybacks, but I seldom get my wish. At a minimum, though, I demand a baseline level of management competency when it comes to capital allocation. I will not invest in securities where there has been a large increase in shares outstanding over the past few years. Given the precarious financial position of many deep value stocks, however, even a competent management team may be forced to issue some shares at fire-sale prices in the absence of other financing options. With a 5.6% growth in share count over the last five years, GIFI clears this hurdle, barely.

Stock is not Trading at 52-week and/or 5-year Highs

GIFI trades off of its 52-week and 5-year highs by a healthy margin. It is worth mentioning, though, that this criteria is less strict than the preceding three. Typically, a deep value stock with a price at or near 52-week or 5-year highs would indicate a value trap. In addition, stocks which have recently performed poorly, on average, show subsequent superior performance (see “Stocks that Have Declined in Price”). However, there are special cases, like a recent change in capital structure or a turnaround, where a deep value stock can trade near all-time highs and still represent an attractive opportunity.

—----------------

Capital Allocation

Good capital allocation is something quantitative that we can point to as a potential catalyst to remedy a stock’s undervaluation. I would like to see: de-leveraging, share buybacks, dividends (special or regular), insider buying, or pursuit of strategic alternatives. A value-oriented activist investor will push for these types of things, so the mere presence of an activist is also a big plus.

It is reassuring to see that GIFI has a rock-solid balance sheet, which it needs to weather heavy losses over the last few years. The company has started to liquidate its shipbuilding division, which explains the monster cash pile on the balance sheet. This is a positive sign.

—----------------

Valuation

GIFI trades at around 56% of tangible book value. The share price may drift higher if management continues asset sales. However, shares have traded at a discount to book value for the last five years, so I suspect upside may be limited here. The appealing thing about this investment is its apparent downside protection (at least in the short term). We have a stock priced at rock-bottom levels and some intelligent capital allocation moves. I believe this is a favorable risk-reward tradeoff.

—----------------

Disclosure: Long GIFI at time of publication. I have no business relationship with the company. I am not a financial advisor, and this post is not financial advice. This post is for informational purposes only. Readers should conduct their own research. Purchase of any security involves risk of permanent loss of capital.

I like the downside protection on GIFI. Do you expect a turnaround/return to net profit in the future?